Cycle Convergence: Oil, Geopolitics & Crisis Risk

The correctly anticipated Q1 2026 shakeout, as identified by our timing models, underscores a structural repricing underway, rather than a transient bout of macro volatility. It is increasingly shaped by cycle convergence—the interaction of late-cycle economic dynamics, unresolved geopolitical tensions, and reflexive behavioural extremes.

History shows that instability tends to intensify when risks are visible yet unresolved. In such environments, price behaviour drifts from traditional fundamentals and begins to discount credibility, policy capacity, and the probability of discontinuity. The framework echoes the insight of Harvard economist Joseph Schumpeter: capitalism evolves through disruption and renewal, not linear progress.

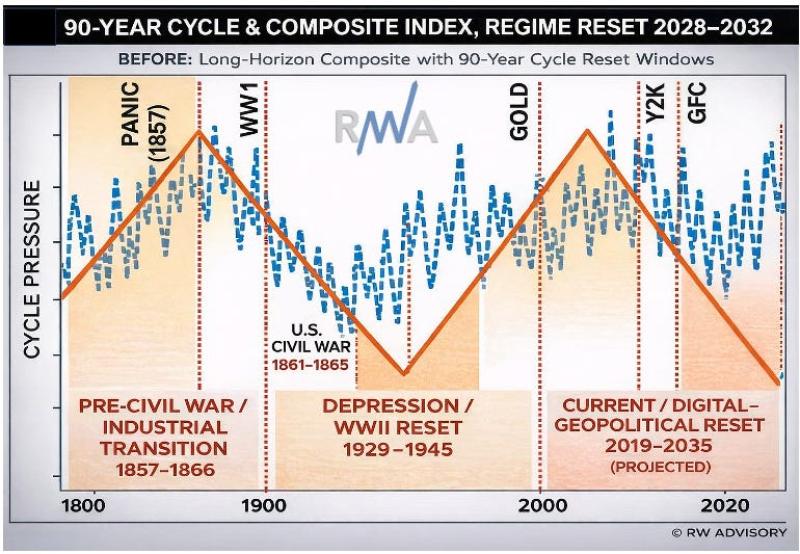

This backdrop fits within a broader super-macro cycle in which hegemonic systems periodically face tests of adaptability. Our expanded cycle framework places the present era in the late stages of a roughly 90-year crisis rhythm, with pressures likely to intensify into the 2026–2032 window as institutional credibility, alliance structures, and economic arrangements come under mounting strain (Figure 1, featured in our latest special macro report: Navigating the 2026 Cycle Convergence).

Earlier crisis eras such as 1857–1866 and 1929–1945, followed similar paths, where financial strain, geopolitical rivalry, and domestic pressure interacting for years before new arrangements consolidated. In the 19th century, the articulation of the Monroe Doctrine signalled an emerging hemispheric order amid imperial competition. After the Second World War, the Bretton Woods framework embedded a U.S.-anchored financial architecture designed to stabilise currencies and expand trade. As those systems matured, however, internal contradictions accumulated and policy tools increasingly shifted toward sanctions, trade controls, and security signalling.

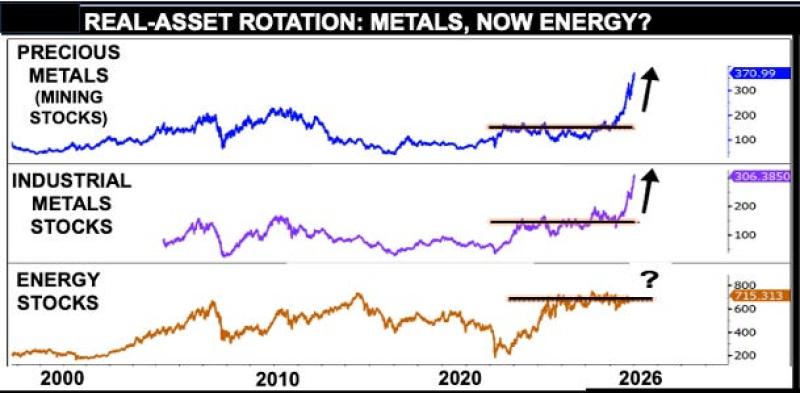

Today’s environment carries similar characteristics. Economic fragmentation, strategic competition, and domestic pressures are again interacting within a system whose institutional foundations are being questioned. Markets are responding accordingly. The earlier phase of late-cycle leadership from precious metals is now broadening toward energy, reflecting a transition from monetary anxiety to concerns about physical supply, security, and enforcement power (Figure 2). Such tools can influence political trajectories—as recently observed in Venezuela—but they also heighten the risk of miscalculation and transmit volatility directly into global commodity markets.

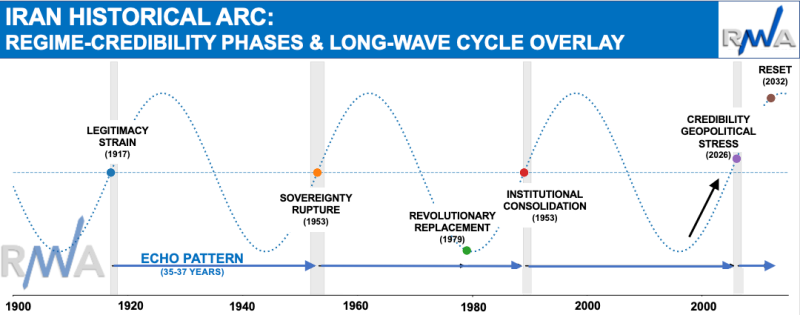

It is within this environment that Iran’s role becomes more consequential. Viewed across longer waves of institutional authority, Iran’s modern history shows a recurring cadence of erosion and consolidation: imperial decline in the early twentieth century, the sovereignty rupture of 1953, revolutionary replacement in 1979, and stabilisation after 1989. By comparison and cyclical pattern (approx 35-37 years), 2026 increasingly resembles another inflection window, where domestic strain and external confrontation begin to intersect (Figure 3).

Markets may not forecast political outcomes, but they respond rapidly when internal fragility risks spilling outward. This is unfolding alongside a broader shift away from a predominantly U.S.-led framework toward a more contested, multipolar environment in which BRICS actors, notably Russia and China, carry greater marginal influence. That combination elevates risks and helps explain the ongoing rotation toward commodities and energy, with normalisation narratives usually emerging only after uncertainty and disruption peaks.

The transmission channel is geography. Iran sits astride the Strait of Hormuz, one of the most critical arteries in the global energy system. When domestic stress converges with wider fragmentation, even marginal shifts in behaviour can have disproportionate effects on expectations, insurance premia, and supply assumptions.

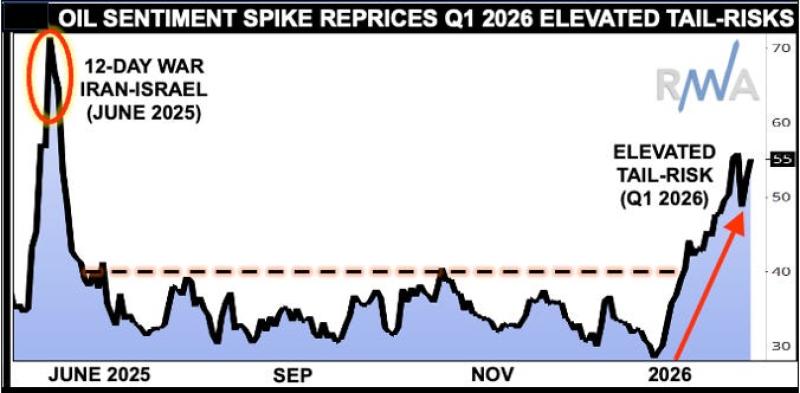

The Q1 cycle stress window is a catalyst for this sensitivity to be re-priced in markets. As crowded exposures elsewhere were liquidated, crude began unwinding from oversold and structurally constrained levels, just as geopolitical optionality increased. This is highlighted in oil’s bullish chart setup (Figure 4) and our Global Ranking Model (GRM). Oil was not merely caught in the risk-off move but instead re-coupled to market-implied tail-risk.

Importantly, this momentum unwind is not merely about portfolio de-risking, AI concerns, or even a change in Fed leadership. It reflects a broader repricing of security of supply in a regime where deterrence credibility, alliance cohesion, and political capacity are all under examination. Under such conditions, energy begins to behave less like a cyclical commodity and more like a strategic asset.

Volatility markets reinforce the signal. Rising option premia suggest preparation for disruption rather than mean reversion; a configuration more typical of geopolitical supply concern than demand weakness. (Figure 5).

The recent interconnected events compound that perception. The 12-Day War, which resulted in a ceasefire that paused escalation without resolving underlying tensions. Thereafter, Iran’s sharp currency depreciation, fuelled in part by U.S. “economic statecraft”, including sanctions and financial pressure, amplifying existing domestic unrest and renewed fears of another U.S. strike.

In this VUCA environment, market myopia has intensified, with investor attention collapsing into variations of a primary risk narrative: Will tensions escalate into a prolonged regional conflict, with systemic implications for the Strait of Hormuz? As a chokepoint for nearly a third of global seaborne oil flows, even partial disruption carries outsized consequences. U.S.-Iran talks now cautiously resume, with both sides offering conditional willingness to engage. Yet negotiations remain fragile, with diplomacy unfolding alongside ongoing military posturing, raising regional tensions and potential risks to the U.S. midterm elections.

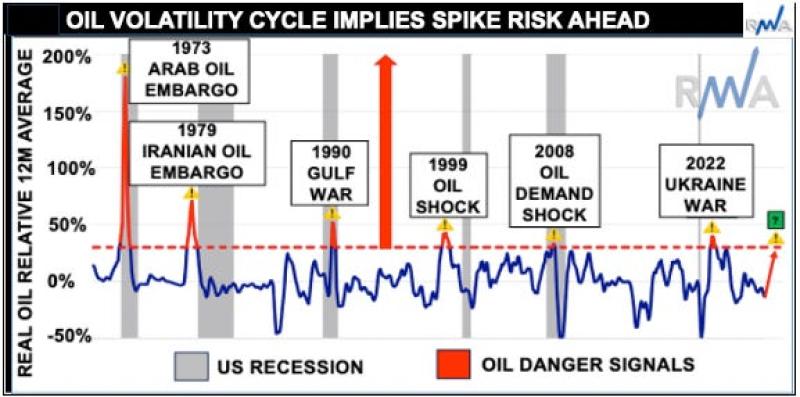

This combination is being interpreted not as de-escalation, but unstable equilibrium. Mr. Market’s behavioural reflexivity remains the critical variable. Strike or no strike, perception dominates pricing, and small probability shifts can produce outsized market responses. Oil’s volatility signature reinforces this concern and, under disruption scenarios, implies scope for renewed spikes toward the $115–120 range (Figure 6). Such outcomes would risk transmitting a stag-flationary impulse through the global economy, encouraging investors to consider pre-empting equity hedges and relatively greater exposure to energy-linked assets.

For investors, the conclusion is straightforward. In convergence regimes, priority shifts from optimisation toward resilience. Capital gravitates toward hard assets, particularly energy—not only for return potential, but as protection against systemic risk.

Select link for more details: https://ronwilliam.substack.com/about

«Cycle Convergence: Oil, Geopolitics & Crisis Risk»