What is happening on the Japanese bond market?

"Our country's fiscal situation is undoubtedly extremely poor, worse than Greece's." In May 2025, speaking before Parliament, Prime Minister Shigeru Ishiba did not mince his words. He argued for rejecting demands for tax cuts funded by more debt, in a context of widespread interest rate rises. This was a rare statement in Japan's culture of consensus.

Bond yields measure a country's credibility

The sovereign bond market—through which governments borrow directly from investors in exchange for a return—is the subject of particular attention. It is considered more rational than the stock market, and daily trading volumes are higher. The interest rate, or the “rent for money” over a given period, acts as a barometer. It measures in real time the financial credibility of a country in the eyes of its creditors.

Sovereign debt offers lower returns than equities, but in exchange for what is considered lower risk. It attracts long-term savings—capital from pension funds, retirement funds, life insurers, and sovereign wealth funds—which favor predictability over performance.

However, two factors can push these rates up. The first is confidence. As Walter Bagehot wrote in Lombard Street: “Credit—the disposition of one man to trust another—is singularly varying.” When it falters, investors demand a higher risk premium to continue lending.

The second factor is inflation. Lending means taking the risk of being repaid in a devalued currency. A rational creditor anticipates this and demands a return higher than expected inflation in order to preserve a positive real return. Thus, the higher inflation expectations are, the higher the required rate.

Bond vigilantes are large holders of debt securities who, when they believe that the risk of default or inflation is increasing, sell off their bonds en masse. This selling pressure causes prices to fall and, mechanically, yields to rise. The market then sends an unambiguous signal to the government concerned: its credibility is at stake and the cost of its debt will increase.

"I used to think that if there was reincarnation, I wanted to come back as the president or the pope or a .400 baseball hitter. But now I want to come back as the bond market. You can intimidate everybody." summarized James Carville, advisor to Bill Clinton, in 1993.

How did the Japanese government get so deeply into debt?

Japan's massive debt is the result of successive debt transfers between economic actors over more than thirty years, in response to repeated crises aimed at preventing a credit bubble from bursting.

The private sector

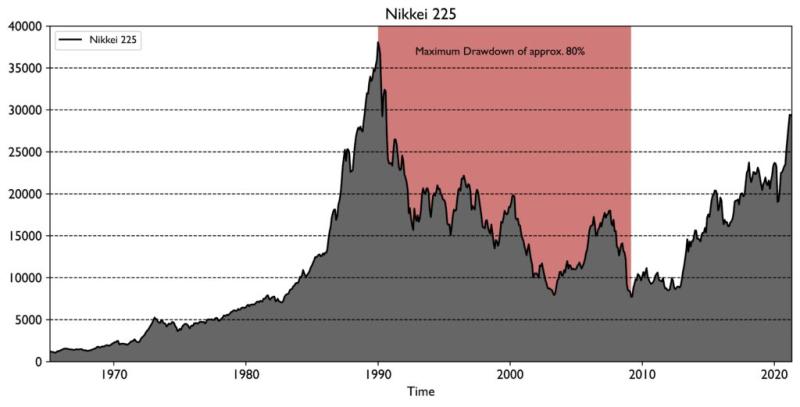

During the 1980s, Japan's economy experienced an unprecedented borrowing frenzy. Households took on debt to purchase real estate, companies borrowed to invest and speculate, and banks granted loans with disconcerting ease. Stock and real estate prices skyrocketed, fueling the famous “Japanese bubble.”

The crash came in 1990 and was brutal: the stock market lost up to 80% of its value, while real estate prices fell by 60 to 70% in major cities. Banks were left with significant bad debts, private consumption and investment collapsed, and deflation set in. It was a vicious circle in which falling prices fueled stagnation. This marked the beginning of the “lost decades.”

The government

Faced with the collapse of private sector economic activity, the government intervened to prevent a depression similar to that of 1929. It launched a series of stimulus plans: major infrastructure projects, support for businesses, and increased social spending in a society marked by an aging population.

These measures were financed by massive issues of government bonds. Public debt, which represented around 60% of GDP in 1990, exceeded 100% in the 2000s. In 2010, it exceeded 200%, then peaked at around 255% of GDP during the Covid crisis before falling back slightly.

This trajectory is unfolding in an environment of extremely low, even negative, inflation, which is conducive to maintaining very low interest rates. The buyers of this debt are mainly domestic: banks, insurers, pension funds, savers—as well as the central bank.

The central bank

The Bank of Japan (BoJ) has been intervening since 2001 through quantitative easing. With private market demand unable to absorb the colossal volumes of bonds issued by the Treasury without causing a sharp rise in rates, the BoJ created money out of thin air to directly repurchase sovereign debt and other financial assets.

This mechanism took on unprecedented proportions from 2013 onwards. The central bank ended up absorbing such large amounts that, at one point, it held nearly half of all outstanding sovereign bonds. Its balance sheet, which stood at around ¥100 trillion in 2000, peaked at nearly ¥750 trillion in 2024—equivalent to the country's annual GDP.

Through its unconventional policy, the BoJ kept interest rates close to zero, or even negative, until 2024, facilitating the refinancing of government debt despite its explosive growth. This policy also contributed to a lasting weakening of the yen, supporting the country's exports.

Why are interest rates rising in Japan?

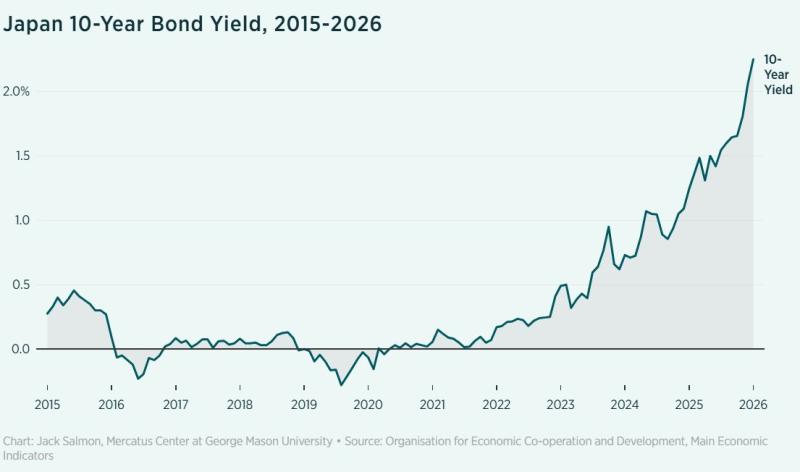

Since 2022, the yield on the Japanese 10-year government bond—the market benchmark, the 10-year JGB—has risen dramatically. It rose from around 0.13% on January 1, 2022, to nearly 2.24% in early 2026, a more than seventeenfold increase in four years. This is an exceptional shift for an economy that has been accustomed to near-zero rates for nearly three decades.

On January 19 and 20, 2026, massive sales of Japanese sovereign bonds triggered a contagion effect on global markets, including the US bond market. 10-year JGBs fell, wiping out approximately $41 billion in value from an estimated $7.2 trillion outstanding. Very long maturities—between 30 and 40 years—were the hardest hit. Their yields jumped by around 25 basis points (0.25%) in a single session to reach over 4.2%.

The rise in rates in Japan can be explained by the return of inflation. The archipelago is heavily dependent on imports for its energy and raw materials. When global prices rise, Japan “imports inflation” into its domestic economy. Inflation now appears to be structural, supported by wage increases, triggering a cycle in which wages and prices reinforce each other.

The second reason is growing concerns about the sustainability of public debt. Highly aggressive fiscal policies—massive stimulus packages, energy subsidies, increased military spending, and electoral support measures—are fueling fears of a sharp increase in debt and additional inflationary pressures. Under the government led by Sanae Takaichi in 2026, this stance reinforced investors' risk premium requirements, causing a sharp rise in long-term interest rates.

In response to the return of inflation, the Bank of Japan began tightening its monetary policy. In other words, it is making credit more expensive. It is raising its key interest rates and gradually implementing quantitative tightening, i.e., reducing its balance sheet by selling bonds it had previously purchased. This increases the supply of bonds on the market, which automatically pushes up rates. The rise in yields then slows economic activity, which helps to curb inflationary pressures.

However, this remedy comes at a major cost: the rise in rates significantly increases the interest burden that the government must pay on its public debt. The more yields rise, the more debt servicing absorbs a significant portion of the budget, which undermines long-term fiscal sustainability.

The BoJ is thus faced with a no-win dilemma. If it allows rates to rise to combat inflation, it risks ultimately triggering a sovereign debt crisis by making its financing unsustainable. But if, on the contrary, it monetizes public debt on a massive scale, it exposes itself to a sharp depreciation of its currency, the yen.

Repatriating assets held abroad

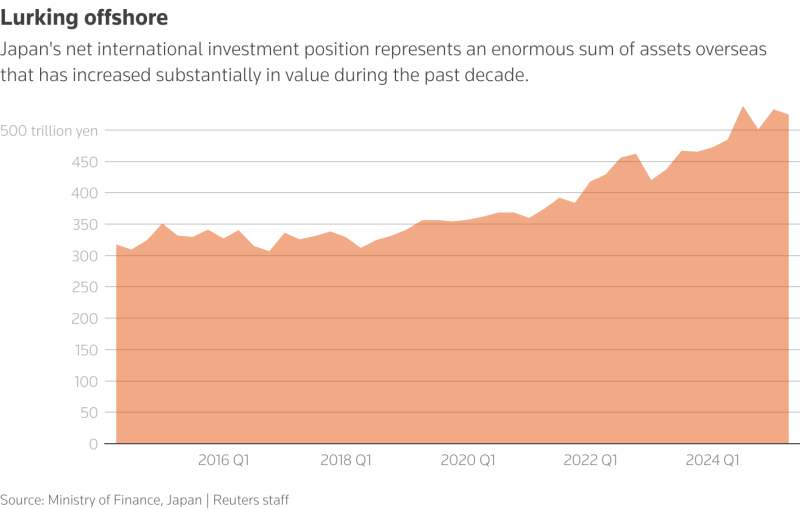

Japan has accumulated a colossal public debt, exceeding 250% of its GDP, while remaining one of the world's leading net creditors. At the end of September 2025, its net foreign investment position stood at around $3.663 trillion.

This external wealth stems in part from decades of current account surpluses: exports and income generated abroad have largely exceeded imports, building up considerable national savings.

The Bank of Japan's ultra-low interest rate policy, maintained for nearly 30 years to contain deflation, has also prompted Japanese investors—banks, insurance companies, pension funds, and individuals—to deploy their capital abroad on a massive scale, acquiring bonds, stocks, and companies, mainly in the United States, Europe, and Asia.

This movement has been amplified by carry trade: borrowing in yen at virtually zero percent to invest in assets offering much higher returns elsewhere. For more than three decades, this mechanism has helped make Japan the world's largest net creditor.

Today, Japanese institutional investors hold between $5 trillion and $7 trillion in foreign assets. Of these, approximately $1.3 trillion is invested in US Treasury bonds maturing at the end of December 2025, making Japan the largest foreign holder of US public debt. The GPIF, the world's largest pension fund, allocates nearly half of its assets to foreign bonds and equities.

But the situation could change as interest rates rise in Japan. Several analysts, notably at Goldman Sachs and HSBC, are anticipating a partial repatriation of these funds to the domestic bond market. Such a move could support demand for JGBs, stabilize their yields, and strengthen the yen.

Nevertheless, the authorities remain cautious: even a limited repatriation could cause sudden adjustments in global markets. These savings, exported for 30 years, now represent a short-term lever lever for public finances and the Japanese currency.

When do we know that a country is bankrupt?

As a country's debt burden increases, striking the right balance on interest rates becomes increasingly perilous. Yields must remain attractive enough to encourage investors to subscribe to new bond issues, without increasing the interest burden to the point where it becomes unsustainable for public finances.

According to Ray Dalio, founder of Bridgewater Associates, a sovereign solvency crisis erupts precisely when rising rates generate significant losses on the balance sheet of the central bank—which holds huge volumes of government bonds. If these losses become too heavy and the institution finds itself facing cash flow problems, it may be forced to create money to absorb them, thereby indirectly monetizing public debt.

The risk then ceases to be purely fiscal and becomes monetary: the money supply increases, the currency depreciates, confidence in its real value erodes—fueling imported inflation and potentially triggering a vicious cycle. For now, the rise in interest rates in Japan is causing accounting losses on the central bank's balance sheet, but without pushing it to resort to massive money creation.

Since the second half of 2025, an anomaly has caught the attention of economists such as Luke Gromen: the yen continues to depreciate against the dollar—reaching nearly 156 JPY/USD in February 2026—even as the yield on 10-year Japanese bonds rose from around 1.8% to over 2.2% at its recent peak, stabilizing around 2.10% in early March.

The chart highlighted by Gromen illustrates this phenomenon: the blue line represents the difference between the yield on 10-year US Treasury bonds and that on 10-year Japanese government bonds (10y UST yield – 10y JGB yield), while the red line corresponds to the USD/JPY exchange rate. Historically, these two curves have shown a strong positive correlation.

Normally, when the yield spread widens—i.e., when US yields move further away from Japanese yields—the yen depreciates because carry trades become more attractive: investors borrow yen at low cost to invest in higher-yielding dollars. Conversely, a narrowing of the spread, i.e., a relative rise in Japanese yields, should logically reduce interest in carry trade and lead to an appreciation of the yen.

However, the recent rise in Japanese yields, which has narrowed the gap with US rates (blue line falling), has not led to the expected appreciation of the yen (red line). This suggests that investors doubt the sustainability of Japanese public debt at these interest rate levels and anticipate intervention by the Bank of Japan to ease the interest burden and restart an inflationary cycle.

Conclusion

For decades, Japan benefited from an exceptional combination of factors: virtually no inflation, extremely low interest rates, accommodative fiscal policy, and massive exports of its savings. These factors long masked the growing fragility of its public finances. Today, with the return of inflation, rising interest rates, and the first signs of market mistrust, the country is entering a period of uncertainty not seen in 30 years. History teaches us that long periods of low interest rates are often just the calm before the storm.

«What is happening on the Japanese bond market?»