Iran is undermining the foundations of the dollar

On February 28, 2026, the United States and Israel launched massive airstrikes against Iran. On the same day, Tehran responded by blocking the Strait of Hormuz, a single strategic passage through which approximately one-fifth of the world’s oil and gas flows.

A month ago, Iran announced the imposition of a toll intended to “secure” the passage of tankers, set at the equivalent of one dollar per barrel.

A supertanker, or VLCC (Very Large Crude Carrier), carries an average of 2 million barrels, which translates into a fee to approximately $2 million per transit, payable in yuan or any currency other than the dollar.

This measure is part of a strategy with major implications: transforming a geographical chokepoint into a genuine instrument of geopolitical and financial power.

Asserting dominance over the Gulf Monarchies

By blocking the Strait of Hormuz, Iran is exerting direct pressure on its regional rivals and reshaping the balance of power of the Middle East. This strategy could shift Tehran from the status of a sanctioned actor to that of a power capable of dictating the rules of regional energy trade.

The figures underscore the stakes. According to the International Energy Agency, the major coastal producers were producing a total of approximately 25.8 million barrels of crude oil per day in 2025: Saudi Arabia (9.51 Mb/d), Iraq (4.39 Mb/d), Iran (4.19 Mb/d), the United Arab Emirates (3.82 Mb/d), Kuwait (2.58 Mb/d), and Qatar (1.31 Mb/d)—accounting for nearly a quarter of global consumption, estimated at 104 million barrels per day, during the same year.

By conditioning these flows, Iran is disrupting the internal balance of OPEC+ and asserting control over its competitors’ exports.

Ending the petrodollar

By introducing a toll in yuan—or any other currency—Iran is challenging a historic barrier: the pricing of oil in dollars. Tehran is leveraging a physical chokepoint—the Strait of Hormuz—to crack its financial counterpart: the dollar’s dominance over the energy trade, which lies at the heart of Washington’s ability to impose sanctions on the rest of the world.

The origins of this system date back to 1974. At the instigation of Henry Kissinger, the United States concluded a secret agreement with Saudi Arabia: Washington guaranteed military security and technological support; Riyadh committed to pricing its oil exclusively in dollars and reinvesting its surpluses in U.S. debt.

The petrodollar is the latest chapter in a historical continuum that dates back to the agreement of February 14, 1945, between Franklin D. Roosevelt and King Ibn Saud aboard the USS Quincy. The Quincy Pact—oil in exchange for security—constitutes one of the foundations of the global energy and monetary order, and permanently anchors the Middle East at the center of U.S. foreign policy.

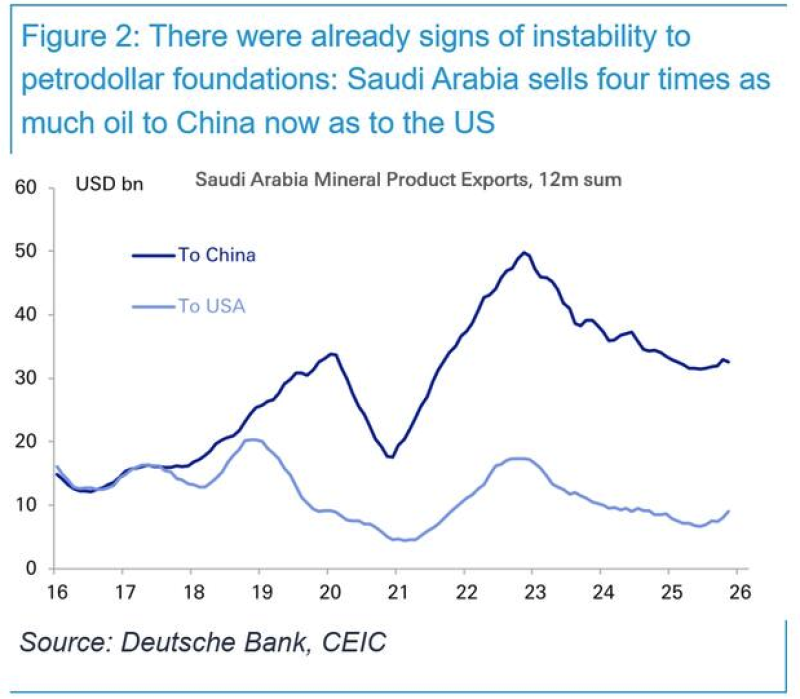

This order persists to this day, despite the fact that the structure of Saudi exports has undergone a profound transformation. According to Deutsche Bank, for every barrel exported to the United States, approximately four are now destined for China. Washington has since become the world’s leading producer thanks to shale oil.

“The Middle East’s considerable strategic importance for the dollar’s role as a global reserve currency should not be underestimated. The current conflict could put the foundations of the petrodollar system to the test,” according to the German bank’s report.

The dollar’s centrality in the region rests primarily on the U.S. military presence. The monetary order is thus closely linked to the security order, which explains why Tehran, alongside its ambitions for de-dollarization, is targeting U.S. military bases and demanding their withdrawal from the region.

Tehran is not alone in wanting to de-dollarize the world

Tehran is not acting in a strategic vacuum. Russia and China are each, in their own way, pursuing a converging goal: reducing their exposure to a dollar-dominated financial system—and to the resulting U.S. sanctions.

The turning point came in 2022. The freezing of the Russian Central Bank’s assets—nearly $300 billion—set a historic precedent. In the space of a single day, the world’s third-largest military power saw a substantial portion of its foreign exchange reserves rendered unusable by a coordinated administrative decision by Western powers.

China has not (yet) suffered a comparable shock, but since 2018 it has faced a gradual escalation of U.S. restrictions: targeted sanctions, export controls, and technological pressure.

U.S. sanctions, overseen by OFAC (Office of Foreign Assets Control), rely on the Western banking network and, more specifically, on correspondent banks. These institutions—such as JPMorgan Chase, Citigroup, HSBC, BNP Paribas, and Deutsche Bank—serve as intermediaries in international payments between banks that do not have direct relationships, particularly for dollar-denominated transactions. They do more than simply facilitate the flow of funds: they are the ones who directly enforce the sanctions and become, de facto, the enforcement arm of U.S. foreign policy.

And if that is not enough, the United States leverages SWIFT, the Brussels-based international financial messaging system, which facilitates the majority of cross-border payments. Excluding a country from it amounts, de facto, to isolating it from international trade.

Faced with this vulnerability, Beijing is building a parallel system. On one hand, the mBridge project, developed by several central banks (including those of Hong Kong, the United Arab Emirates, and Thailand), explores the use of central bank digital currencies to settle international payments directly between states, bypassing traditional banking channels.

On the other hand, the Cross-Border Interbank Payment System (CIPS), an international payment system launched by China in 2015 to facilitate cross-border transactions in yuan, partially bypassing SWIFT.

The yuan’s Achilles’ heel… and how to work around it

Despite the establishment of an increasingly independent financial infrastructure—through CIPS and projects like mBridge—the yuan remains an imperfect currency for international trade. It is not freely convertible. China maintains strict controls on capital flows, and the People’s Bank of China (PBOC) actively manages its exchange rate.

For now, Beijing is internationalizing the yuan primarily through two channels. First, by expanding trade settled directly in yuan. Second, by developing offshore yuan financial markets located outside China (notably in Hong Kong).

Many observers also highlight China’s desire to develop a complementary mechanism: gold as an exit asset. Through the Shanghai Gold Exchange, Beijing has established a market that theoretically enables a form of gold-yuan convertibility. Thus, a yuan holder is not necessarily forced to hold a currency that is still not widely internationalized; under certain conditions, they can reallocate these assets into gold.

Without making the yuan fully freely convertible, Beijing is thus facilitating a form of recycling of surpluses into a real and neutral asset, shielded from U.S. sanctions. This mechanism does not eliminate trade imbalances, but it reduces the tensions associated with the accumulation of yuan liquidity.

China’s de-dollarization strategy thus rests on three pillars: alternative payment systems (CIPS and similar projects), the gradual internationalization of the yuan, and the potential role of gold as a buffer.

It all comes down to the margin

Many observers may consider Iran’s demands are unfeasible, or even symbolic: billing the equivalent of one dollar per barrel in yuan would not, on its own, be enough to erode the dollar’s hegemony.

It is estimated that before this war, approximately 20% of the world’s oil was already traded in a currency other than the dollar. The share denominated in yuan remains limited today, at around 6 to 7%. This seems marginal at first glance, but this proportion was still virtually zero five years ago.

In finance, prices are not determined by total trading volumes, but rather, at the margin, by the latest transactions between marginal buyers and sellers. These transactions set market prices.

The same mechanism is at work in the U.S. sovereign debt market. Interest rates are largely influenced by marginal buyers.

Consequently, if a growing share of global trade gradually moves away from the dollar, and if the corresponding trade surpluses are no longer automatically channeled into dollar-denominated assets—particularly U.S. Treasury bonds—then the structural demand for these securities will contract.

Such a development would be difficult to sustain for an economy whose public debt now exceeds 120% of GDP: every rise in rates translates into hundreds of billions of dollars in additional interest costs, which in turn exacerbates the deficits it is supposed to finance.

In this context, former Treasury Secretary Henry Paulson recently called, in an interview with Bloomberg, for the implementation of an emergency plan—a “break-the-glass plan”—to address a potential shock to demand for Treasury bonds, a scenario he himself describes as “disastrous.”

For the past ten years, the BRICS nations have held a series of summits and issued declarations of intent, without bringing about any real transformation of the international monetary system. This new war in the Middle East could, however, act as a catalyst and weaken the petrodollar, one of the pillars of American power.

«Iran is undermining the foundations of the dollar»